LDES Cap & Floor: Ofgem reveals the 16 projects set to shape the UK’s storage future

Against a backdrop of war in the Middle East, climate change driven heatwaves and volatile energy prices, the drive to increase the UK's Long Duration Energy Storage or "LDES" capacity continues apace. On 26 June 2026, Ofgem published its long-awaited shortlist of projects that had successfully made it through the Project Assessment phase of its new Cap and Floor Scheme ("C&F"). See our articles here and here, where we have written previously on this subject.

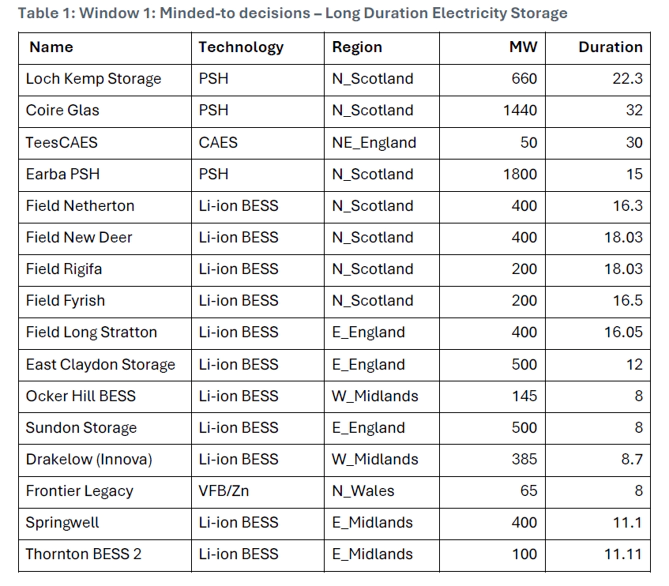

The resulting list shows that Ofgem is 'minded to' award C&F contracts to 16 out of the 73 projects that were assessed (4 dropped out since the initial list of 77 was published), which equates to a total capacity of 7,645MW - at the upper end of NESO's recommended capacity range. The regulator has deliberately procured additional capacity to allow for project attrition while maintaining security of supply objectives.

Ofgem has launched a consultation asking for responses on its methodology before it finalises the list of successful projects this coming autumn. This consultation will close on 7 August 2026.

What made the cut

The full list (reproduced below) shows that lithium-ion BESS continues to dominate, comprising 11 out of the 16 on the shortlist, with a strong showing for Field Energy which has secured 5 spots for its BESS projects. The predominance of BESS does once again raise the question about the design of the scheme which was initially understood to be targeting more typical 'long duration' technologies such as pumped hydro ("PSH"). Although typical BESS systems have a discharge time of around 2 hours, the shortlisted projects have satisfied Ofgem that they can meet (and in some cases far exceed) the 8 hour minimum threshold set in the MCA Framework (Ofgem's assessment framework).

The remaining projects comprise three PSH projects, one vanadium flow/zinc battery project ("VFB/Zn") and what will be the UK's first Compressed Air Energy Storage system ("CAES"). For more on these technologies, read our previous discussion here.

The inclusion of the Frontier VFB/Zn project is particularly interesting because Ofgem notes in its 'Window 1 – Minded-to decisions' consultation document that discretion was applied to specifically increase the diversity of the pool of technologies by granting a place to the best performing VFB project (although it insists that no project has been included on diversity grounds alone). This does suggest that the 'technology agnostic' approach that Ofgem have adopted is failing to produce the desired technological diversity without intervention.

The current sift does also indicate a preference for proven technologies, given that lithium-ion BESS and PSH collectively make up 88% of the pot, with CAES and VFB/ZN comprising the only two next-generation technologies.

How the projects were assessed

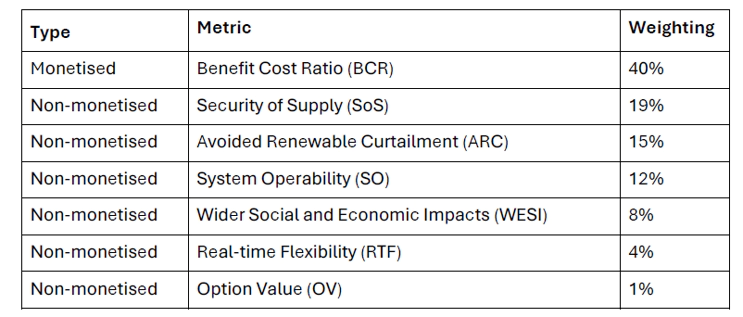

The decisions have been based broadly on a three-part assessment, using the Economic Assessment as the starting point to produce an initial list. This gives each project a ranking from 1 to 73. The Financial Assessment and Strategic Assessments are then applied in turn, modifying the initial ranking each time in order to ascertain the top-performing projects. This means that the cost/benefit ratio of a project forms the bulk of its score (40% weighting), with the focus being on which projects bring overall greatest economic benefit to the system, as well as non-monetised impacts that are difficult to quantify but are essential for the future of UK energy. Security of supply and avoided renewable curtailment make up the top two non-monetised impacts (19% and 15% respectively).

The Financial Assessment focuses on the projects' relative revenue risk (i.e. their projected impact on the cap and floor) with any projects that indicate a propensity to fall consistently below the floor receiving a negative score. The Strategic Assessment looks at other factors not already assessed, such as deliverability, diversity of technology and future scenario sensitivities.

It is notable that Ofgem has taken an investor-friendly approach and decided not to filter out projects based solely on either deliverability risk or grid queue position (provided that a timely pathway to connection is viable) and has instead taken the approach of managing these risks through conditions that would be attached to the award of a contract. The rationale is that to exclude projects based on these criteria alone may come at the cost of what would otherwise be a strong project, whilst conditions and ongoing milestones allow Ofgem to maintain overall accountability.

The types of conditions that are being considered are:

- Evidence of finance-ability and commitment

- Regulatory compliance

- Securing necessary consents

- Applicable design requirements

Looking ahead

The C&F continues to be a significant and necessary step towards achieving the UK's Clean Power 2030 Action Plan, net zero by 2050, and the country's necessary energy security. Its progress will be particularly welcome for bill payers following the government's recent decision not to take on radical reform of the UK energy market or to introduce zonal pricing, as it will provide another tool in the government's toolkit to bring down energy prices in the long term.

Ofgem confirmed that it intends to run future application windows – subject to consultation - with a second window due to open in 2027 (which will be informed by evidence from Strategic Spatial Energy Planning ("SSEP")). In a bid to improve investor confidence, there is likely to be a means to streamline the application process for projects which were unsuccessful under the first window but would like to apply again in subsequent windows (although there will be no passported route for such projects). It will be interesting to follow how the scheme evolves and to see whether future windows will produce a prevalence of advanced lithium-ion technologies (rather than novel alternatives like VFBs, sodium-ion batteries, CAES or Liquid Air Energy Storage), given how well lithium-ion BESS has done in the first round. However, as the scheme is still in its infancy, the methodology is liable to change for future windows based on the evolving energy landscape in the UK, and if there ends up being a glut of long duration lithium-ion BESS technologies to mirror the comparable saturation of short duration BESS, this fact may start to have a negative impact on future entrants when their relative benefits are weighed in future windows.

This announcement also comes hot on the heels of GEMA's success in the case brought against it by Zenobe, a leading BESS developer, that the C&F was an unlawful subsidy scheme and would undercut producers of non-C&F supported BESS. Although the court found against the developer, the decision of the Competition Appeal Tribunal was confined to whether it was an unlawful subsidy scheme, and the case was not considered on general public law grounds.

It is important to note that Ofgem's list of projects is at this stage only 'minded-to' decisions and is now subject to open consultation, after which we could see amendments to the methodology, the list of preferred projects, or both. Those wishing to have their say in the design of the scheme should review the associated documents and complete the online survey by 7 August 2026.

Get in touch

Trainee Solicitor

Related