The recent Budget introduced some significant changes to inheritance tax (IHT), bringing pension funds into the scope of IHT and reducing the impact of Business Property Relief (BPR) and Agricultural Property Relief (APR).

Coupled with a continued freeze in both the nil rate band and residence nil rate band, these changes are likely to substantially increase the IHT revenue in the coming years, with the Office for Budget Responsibility (OBR) forecasting an additional £2bn a year by 2029.

For those with philanthropic intentions, the changes may make leaving charitable legacies all the more appealing, given how tax efficient such a gift can be.

This can mean that in some cases, for every £100 left to charity, the amount received by the other beneficiaries collectively is only reduced by £24 with the IHT liability reduced by £76.

This article explains how gifts to charity can be made in a will, why they can be so tax efficient, and some key points to consider. For more information about giving to charity during your lifetime or setting up your own charity, check out our helpful article.

How can I give to charity via my will?

It is important to first make the point that in order to direct that gifts are made to charity, it is necessary to have a valid will. In the absence of a will your personal representatives follow a prescribed set of rules as to who benefits from your estate.

If you currently have a will that does not include any such gifts, a new will can be prepared that includes them, and this will supersede the old will. It is possible for beneficiaries to vary a will to include a gift to charity, but this should not be relied upon.

A charitable gift can be made in a number of different ways in a will:

- A pecuniary (money) legacy – leaving a specific sum of money – e.g. £1,000.

- A specific legacy – leaving a specific item – e.g. a property or piece of land.

- A residual legacy – leaving a portion of your entire residual estate to charity or charities. Your residual estate is the value left after all pecuniary and specific gifts are made, and all liabilities paid (debts, funeral expenses, IHT etc).

When and how can a legacy be tax efficient?

Tax efficiencies can be found in situations where your estate would otherwise be subject to inheritance tax. For certain estates, the IHT position may change in April 2026 (BPR/APR changes) and again in April 2027 (pension changes) and so this should be factored into any decisions made.

The tax efficiency is generated for two reasons:

- Donations to charity are themselves not subject to inheritance tax.

- If you give at least 10% of your 'Baseline amount' to charity, the inheritance tax rate applying to the remainder of your taxable estate reduces from 40% to 36%.

The 'baseline amount' can be summarised as the total value of your estate (including any BPR/APR assets), less estate liabilities and available nil rate bands.

How does this work?

Understanding how charitable giving could help make your estate more tax efficient can be complex, so we have created the below example.

Joe dies in July 2025 aged 80, owning his home and some investments. His wife Claudia died 3 years ago leaving all her assets to Joe. They have two children Tom and Sarah. Neither Joe or Claudia have made any lifetime gifts above their £3,000 a year allowance. Joe can use both his and Claudia's nil rate band but does not qualify for the residence nil rate band.

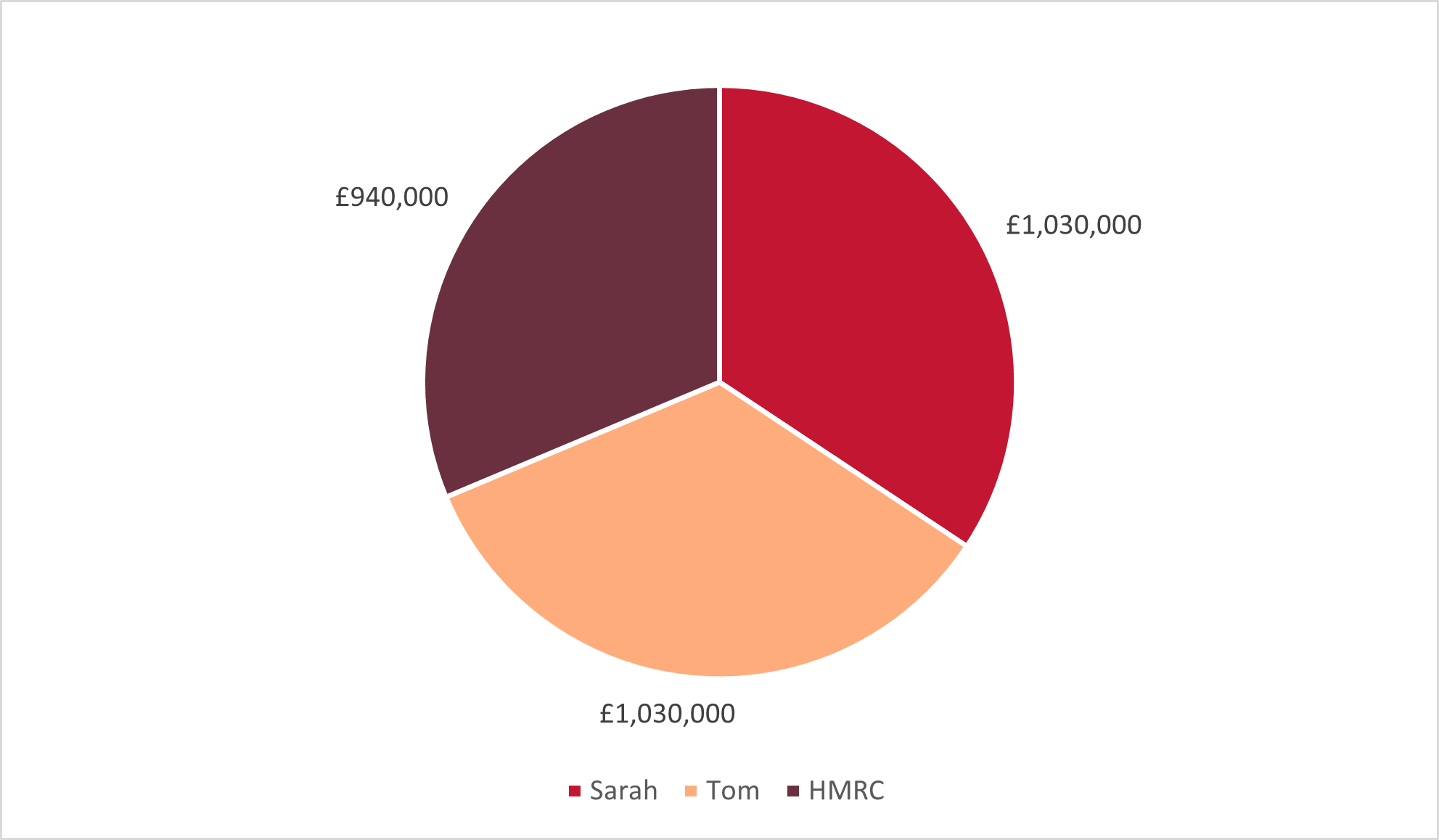

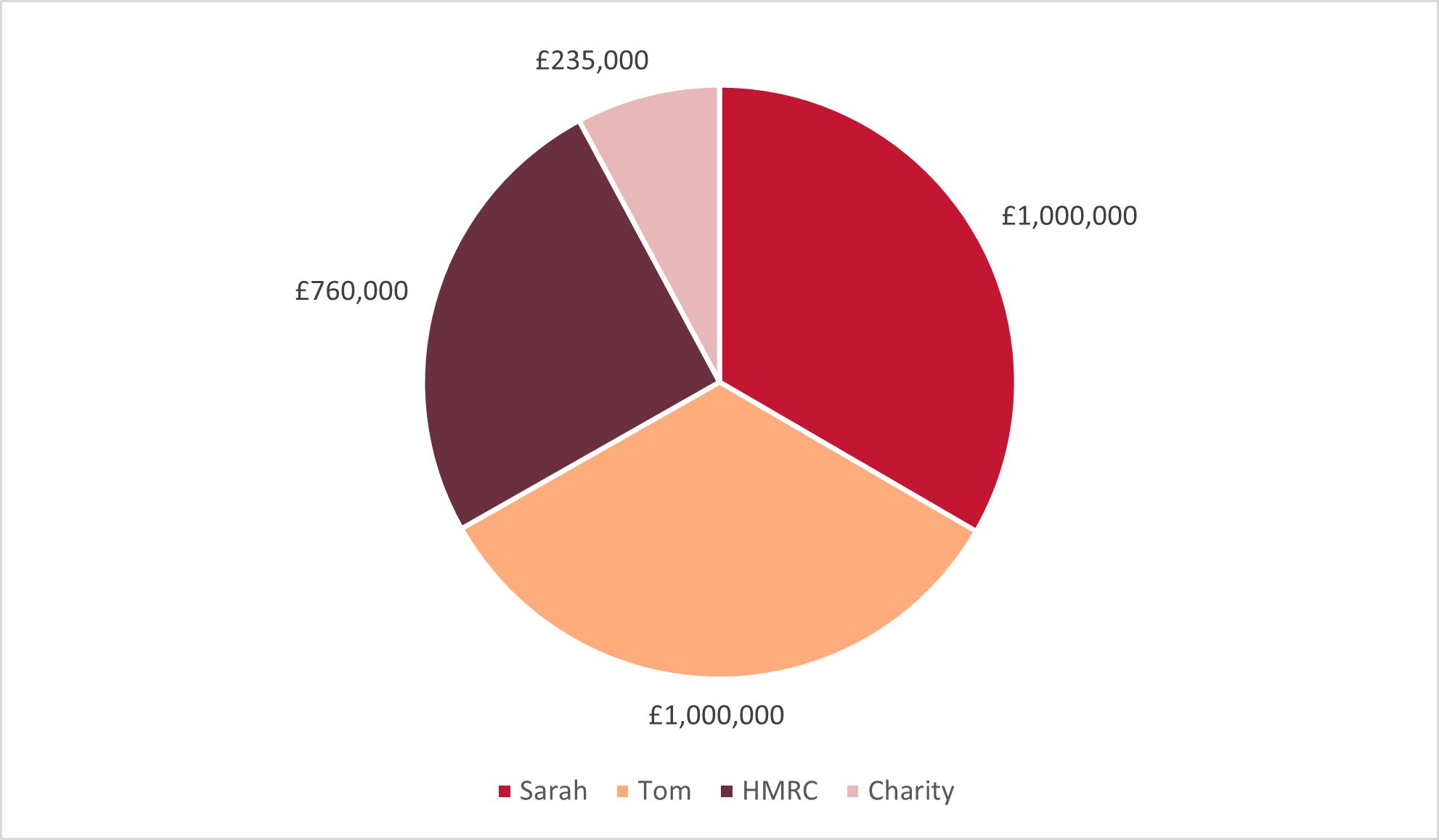

Joe's estate is valued at £3m and he has available allowances of £650,000. The chart below shows how much his children would receive, after tax, with no gift to charity, and with a gift to charity of £235,000 (being 10% of his 'baseline amount' and so the minimum required to access the 36% rate in this scenario).

With no gift to charity:

With a gift of £235,000:

This illustrates how large a tax saving can be obtained with an appropriate level of donation, and the minimal impact on the amount received by beneficiaries.

This can require careful planning depending on the level and type of assets that you hold at death and the manner in which they are held. Where there are a number of gifts made, or your estate includes an interest in a trust, the calculation can be complex, as this article considers.

Key points to consider

It must be clear which charity or charities you are intending to benefit. As this article makes clear where there are doubts the gift can lapse (with the charity receiving nothing), "the best practice would be to include a registered charity number, the correct address and name of the charity as of the date of the will as per its details on the Charity Commission Website".

It is also sensible to add provisions describing what you would like to happen if the charity no longer exists at the time of your death, for example proposing an alternative charity.

Your will would need to state the specific asset or cash amount that you would like to give, if making a pecuniary or specific legacy. To ensure that the reduced rate of IHT is available, specific wording can be included in a pecuniary legacy to direct that a sufficient amount passes to the charity.

Good advice is paramount and our Private Wealth and Legacy specialists will work together to ensure the right outcome as part of your planning.

Key contacts

Principal Director

International Succession & Tax | Owner Managed Businesses | Private Wealth

Related

Articles